Why this question matters

Most Indian investors face the same dilemma — should you invest a lumpsum when you have it, or stagger it through SIPs? Both work, but the right choice depends on your income pattern, market view and discipline.

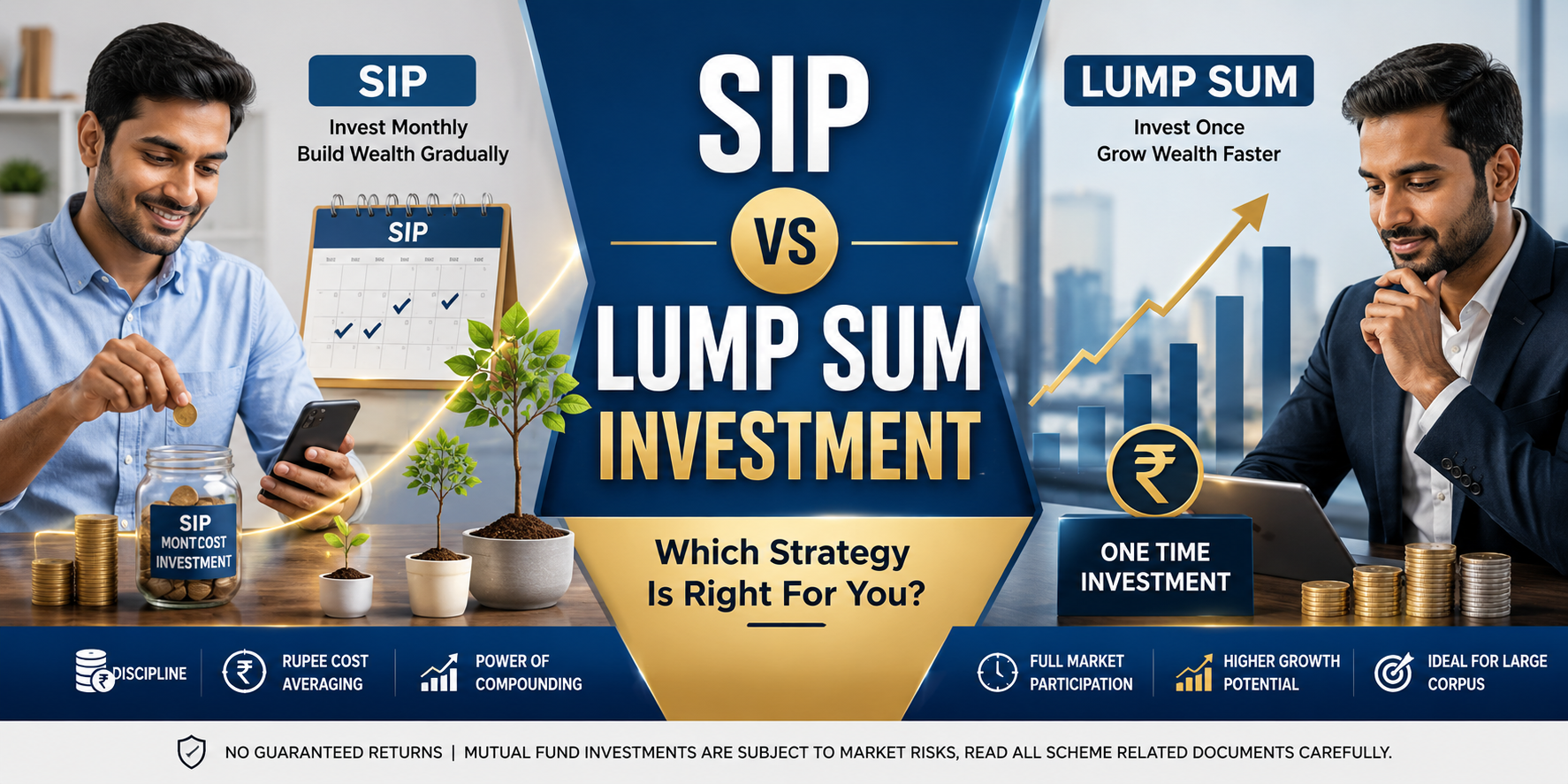

How SIP works

A Systematic Investment Plan invests a fixed amount every month. You buy more units when markets fall and fewer when they rise — this is rupee-cost averaging. Over a full market cycle, your average cost per unit usually lands below the market's average price.

How lumpsum works

A lumpsum deploys your entire amount on day one. If the market trends up, lumpsum almost always wins because every rupee compounds for longer. The risk: a sharp drawdown right after you invest.

A simple rule of thumb

- Salary income → SIP. You're already averaging by design.

- Bonus, inheritance or property sale → STP (Systematic Transfer Plan) from a liquid fund into equity over 6–12 months.

- Volatile markets or near all-time highs → split lumpsum into tranches.

What we recommend at Bhavya Investments

For most families, a core monthly SIP plus opportunistic top-ups during 10%+ corrections gives the best balance of discipline and return. Talk to us before you deploy any lumpsum above ₹5 lakh.